Trending Coins and Tokens🔥

Crypto

Exchange

DeFi 2.0 in 2026: How Decentralized Finance Matured Into Real Financial Infrastructure

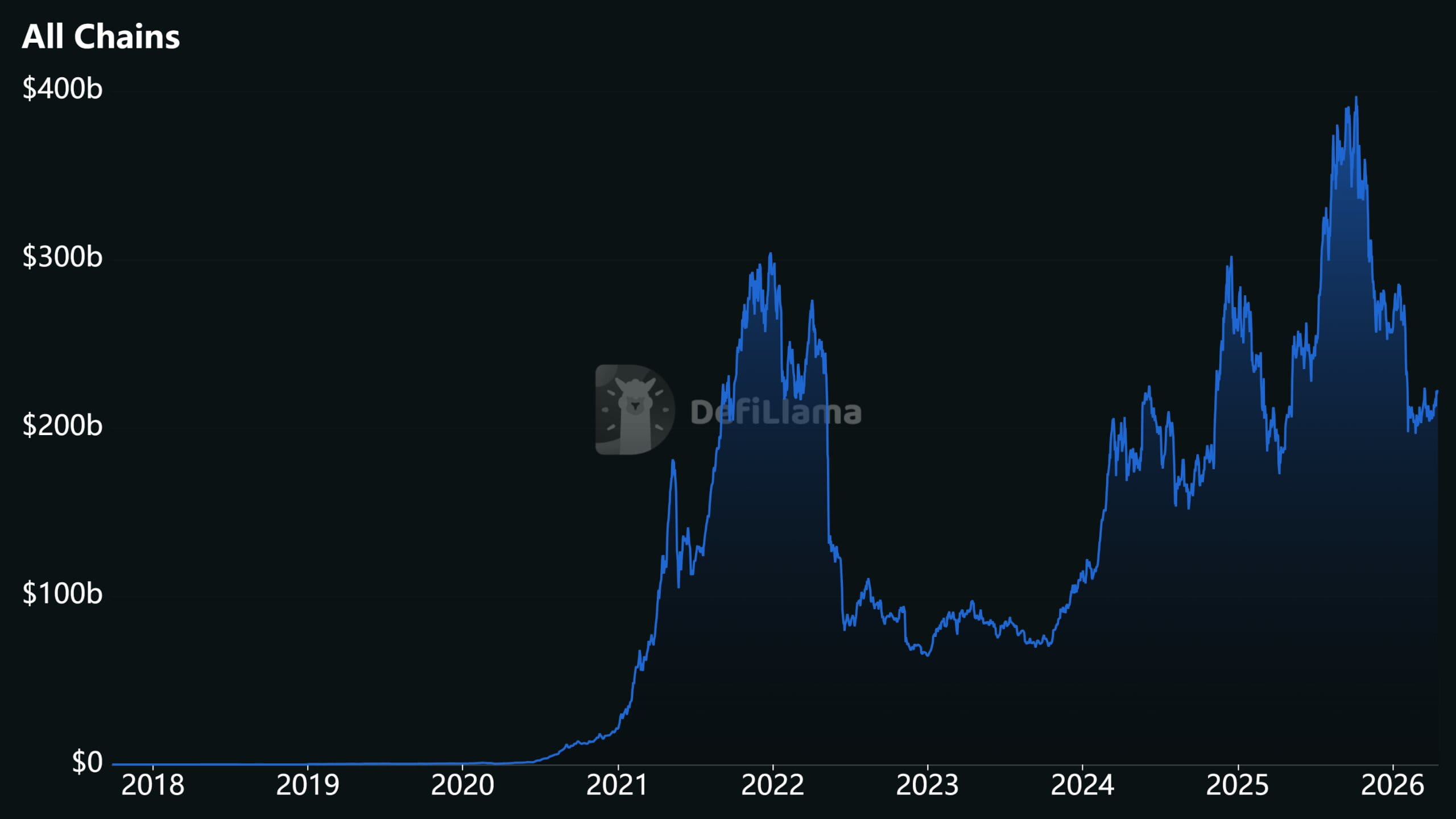

When DeFi 2.0 first entered the lexicon around late 2021, the label mostly pointed to one idea: protocols owning their own liquidity instead of renting it from yield farmers and other external sources. Four years on, the category has outgrown that narrow definition. By early 2026, decentralized finance has rebuilt itself into something closer to parallel market infrastructure, with around $220 billion locked across protocols, institutional treasuries sitting on tokenized Treasuries, and onchain perpetual futures capturing a growing slice of global derivatives volume.

This revised guide rewrites our original piece with current data, new project leaders, and the regulatory shifts that now shape how builders, traders, and institutions interact with onchain finance.

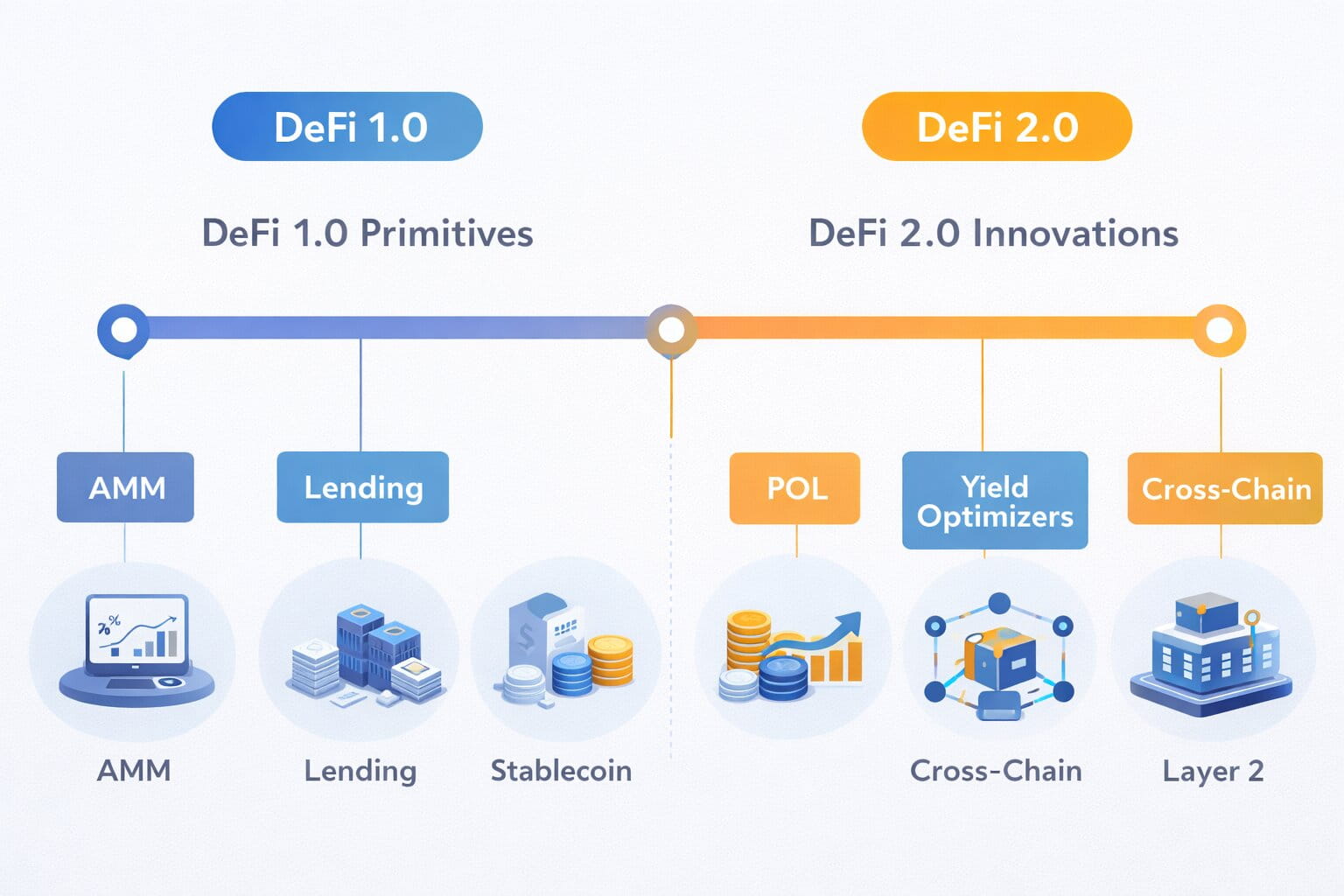

From DeFi 1.0 to DeFi 2.0: A Short Recap

DeFi 1.0 gave the industry its primitives. Uniswap proved that automated market makers could replace order books for basic swaps. Compound and Aave showed that permissionless lending could function at scale. MakerDAO, now operating as Sky, introduced a crypto-collateralized stablecoin that survived multiple market cycles.

The problems were just as clear. Gas fees on Ethereum spiked during volatile periods. Liquidity providers carried impermanent loss. Interfaces assumed a level of technical knowledge most users did not have. Smart contract exploits drained treasuries that had no recourse.

DeFi 2.0 was the response. It tried to fix the liquidity, incentive, and capital efficiency problems of the first generation. The two anchor ideas were Protocol Owned Liquidity (POL), popularised by OlympusDAO's bonding mechanism (see Olympus Docs), and Liquidity as a Service, explored by Tokemak through its liquidity director model. Both aimed to reduce reliance on mercenary capital that would leave the moment a new farm paid better. During this period, Layer 2 solutions focused on and resolved the high fee costs and scalability problems.

Where DeFi 2.0 Actually Stands in 2026

The honest answer is that the 2.0 label has become less useful. The ideas it described, sustainable liquidity, better yield, capital efficiency, got absorbed into DeFi as a whole. What matters now is how the sector has grown up.

A few numbers set the scene as of Q1 2026:

- Total DeFi TVL sits in the $220 billion range, recovering from a post-FTX low near $50 billion but still below peak bull-cycle levels per CoinLaw and live data on DefiLlama.

- Onchain lending has expanded materially, with outstanding loans across major venues up roughly 37 percent year to date through late 2025 (The Block 2026 DeFi Outlook).

- Tokenized real-world assets, excluding stablecoins, range from $19 billion to $36 billion depending on methodology (KuCoin RWA report), with tokenized public-market RWAs alone tripling to around $16.7 billion (The Block).

- Stablecoin supply has crossed $300 billion, and regulatory frameworks in the US and EU now define who can issue them and under what conditions (CoinNewsSpan).

- Decentralized perpetual futures captured about 10 percent of global perp volume by January 2026, up from 2 percent two years earlier (BeInCrypto / CoinGecko report

The story is less "DeFi 2.0 replaces DeFi 1.0" and more "DeFi grew revenue, regulation, and real users." Someone constantly immersed in the system might struggle to notice this transformation, but a careful outside observer cannot miss these remarkable leaps. Capital markets don't measure health by assets under custody alone, and DeFi analysts are increasingly focused on revenue density, the ratio of actual protocol fees to the capital a protocol holds, rather than raw TVL (FinTech Weekly). Total DeFi TVL may also look modest today compared to its 2022 peak of $300B, but it's worth remembering that period marked the top of a bull market, while we are currently in a bear market.

The Core Innovations That Defined DeFi 2.0

Before moving into current projects, it is worth naming the ideas that shaped this phase, because they still matter.

Protocol Owned Liquidity. Instead of paying yield farmers to provide liquidity that vanishes the moment incentives fall, protocols accumulate their own LP positions through mechanisms like bonding. OlympusDAO introduced the model, and variants now run across dozens of treasuries (Olympus Docs).

Liquidity as a Service. Specialized protocols coordinate where liquidity goes. Tokemak's reactors and liquidity directors, and later vote-escrow systems on Curve and Convex, let projects buy liquidity flows instead of bootstrapping pools from scratch.

Layer 2 scaling. Arbitrum, Optimism, Base, zkSync, Linea and Starknet absorbed most of Ethereum's transactional load. Costs fell, but liquidity fragmented across rollups, creating a new problem that intent layers and cross-chain messaging protocols now try to solve (Symbiosis: DeFi in 2025 to 2026).

Cross-chain interoperability. LayerZero, Wormhole, Chainlink CCIP and Hyperlane became standard infrastructure for moving messages and assets between chains, enabling use cases like borrowing on one chain against collateral posted on another.

Yield optimization and rate markets. Pendle, Yearn and other protocols turned variable yields into tradeable fixed-rate and fixed-term products, giving DeFi its own version of onchain fixed income (DL News: State of DeFi 2025).

Real World Assets: Tokenized Treasuries lead the category, with BlackRock's BUIDL and Ondo's OUSG/USDY bringing short-duration U.S. government debt fully onchain. Beyond fixed income, tokenized gold (PAXG, XAUT) now settles billions in volume, tokenized equities are live on platforms like Backed and Ondo's Global Markets, and private credit protocols such as Maple and Centrifuge channel real borrower cashflows into DeFi yields.

Leading Projects Driving DeFi in 2026

The protocol list has changed slightly since 2022, leading protocols are still there but new innovative protocols have emerged. Here is what actually runs the sector today.

Aave is still the dominant lending venue onchain (see Aave and other top Lending Protocols). Its share of total DeFi debt rose from 52.0 percent to 56.5 percent through 2025 (The Block)

Aave v4 officially launched on Ethereum mainnet on March 30, 2026, announced at EthCC in Cannes after more than two years of development (The Block). The key architectural change is a Hub and Spoke design that separates a central liquidity pool from independent Spoke markets, each with its own collateral rules, risk parameters, and liquidation logic, so new lending environments can tap Aave's existing liquidity from day one instead of bootstrapping their own deposit base.

V4 launched with three Hubs, Core, Prime, and Plus, covering risk-adjusted, low-risk, and higher-return stablecoin strategies, and with dedicated Spokes from Lido, EtherFi, Kelp, Ethena, and Lombard.

Aave Horizon, a permissioned RWA lending venue, uses tokenized Treasuries as collateral for stablecoin loans (Ancilar / Medium).

Hyperliquid turned onchain derivatives into a real market. By April 2026 it controlls around 44 percent of decentralized perpetual futures volume and over 70 percent of open interest across perp DEXs, with annual trading volume reaching roughly $2.6 trillion in 2025, surpassing Coinbase's $1.4 trillion (MEXC)

The October 10 event also acted as a catalyst, accelerating its growth. Hyperliquid stole significant market share from CEXs, particularly large centralized exchanges like Binance, and attracted hundreds of thousands of users to its decentralized perpetual trading platform.

Its HIP-3 framework lets third parties launch permissionless perpetual markets for any asset with a price feed, and its HYPE token uses a deflationary buyback-and-burn model funded by a 97 percent protocol fee allocation (BlockEden). Only 7 of Hyperliquid's top 30 markets are crypto pairs; the rest include oil, silver, gold, the S&P 500, and pre-IPO equities like SpaceX and Anthropic.

EigenCloud (previously EigenLayer) (Restaking)

EigenLayer created the restaking category. As of early 2026 it holds approximately $19.7 billion in TVL with more than 4.6 million ETH committed (ChainUp), representing about 68 percent of the $26 billion restaking market (CoinLaw). Its Actively Validated Services (AVS) model lets developers rent Ethereum's economic security to power data availability layers, oracles, shared sequencers and verifiable AI compute. Liquid restaking tokens (LRTs) from ether.fi, Renzo and Kelp DAO account for over $10 billion of the total and remain the preferred way most users participate (BlockEden).

Ondo Finance and BlackRock BUIDL (RWA)

Tokenized Treasuries are the category that dragged institutional money onchain. BlackRock's BUIDL fund now serves as a reserve asset underpinning a new class of onchain cash products. Ondo Finance's OUSG and USDY products, which track short-term US government securities, passed $2.5 billion in combined TVL at peak (KuCoin RWA). Anemoy's JAAA, seeded by Grove inside the Sky ecosystem, reached $1.0 billion in AUM by late 2025 offering onchain exposure to AAA-rated CLO tranches (The Block). Tokenized US Treasuries alone have grown to over $9 to $11 billion in onchain value by early 2026.

Uniswap v4 introduced hooks, which allow developers to attach custom logic like dynamic fees, TWAP automation and onchain limit orders directly to liquidity pool contracts. This shifts the DEX from being a fixed product to an extensible platform (Symbiosis). Uniswap's monthly spot volume crossed $0.5 trillion in the six months between August 2025 and January 2026, putting it among the top ten exchanges globally including CEXs (BeInCrypto).

The rebrand from Maker to Sky came with a broader product suite, including Spark savings products and Grove's institutional credit infrastructure. DAI remains the most battle-tested decentralized stablecoin, and Sky's treasury has become one of the largest allocators to tokenized RWAs in DeFi (DL News).

Pendle enables duration trading and fixed-rate exposure on yield-bearing assets. It is central to how sophisticated users express rate views onchain, and it has increasingly become the venue where yield-bearing stablecoin positions get split into principal and yield components (DL News).

Olympus remains operational and continues to develop its POL model, including Cooler Loans, which let OHM holders borrow against treasury-backed collateral at a 0.5 percent annualized fixed interest rate with no liquidation risk tied to market price (Olympus Docs). Its narrative influence far exceeds its current market cap, but the bonding mechanism it popularized remains in use across dozens of protocols.

The Narratives Now Driving DeFi

The headlines of 2026 are not about POL anymore (Protocol Owned Liquidity). They are about four converging trends.

Real-World Assets as Core Collateral

RWAs moved from experiment to infrastructure. Tokenized Treasuries, private credit, and institutional fund wrappers scaled quickly, with leadership rotating toward recognized asset managers. The important shift is that DeFi's collateral stack is becoming more dollar-native, more institutionally distributed, and more aligned with familiar fixed-income primitives (DL News). Aave Horizon, Sky's Grove, and Morpho's institutional vaults are the early venues where this plays out.

Liquid Restaking and Shared Security

EigenLayer turned Ethereum into what its founder calls a verifiable cloud, a marketplace for decentralized trust. Restakers earn layered yield by securing multiple services with the same underlying ETH (ChainUp). The trade-off is correlated risk: if one AVS has a catastrophic slashing event, effects can ripple across the stack. Competition between EigenLayer, Symbiotic and Karak is pushing AVS economics toward equilibrium yields (Messari theses via OneKey).

Perpetual DEXs and Onchain Derivatives

This is arguably the most important shift of the past 18 months. Perp DEX monthly volume crossed $1 trillion for the first time in October 2025, and decentralized perps now carry roughly 10 percent of global perpetual futures volume (BlockEden, BeInCrypto). The growth is not just Hyperliquid. Lighter, Aster, EdgeX, Paradex and Jupiter Perps have all captured meaningful share. What matters is that permissionless market listings now include commodities, indices and pre-IPO equities, moving perp DEXs beyond pure crypto exposure (Coincub).

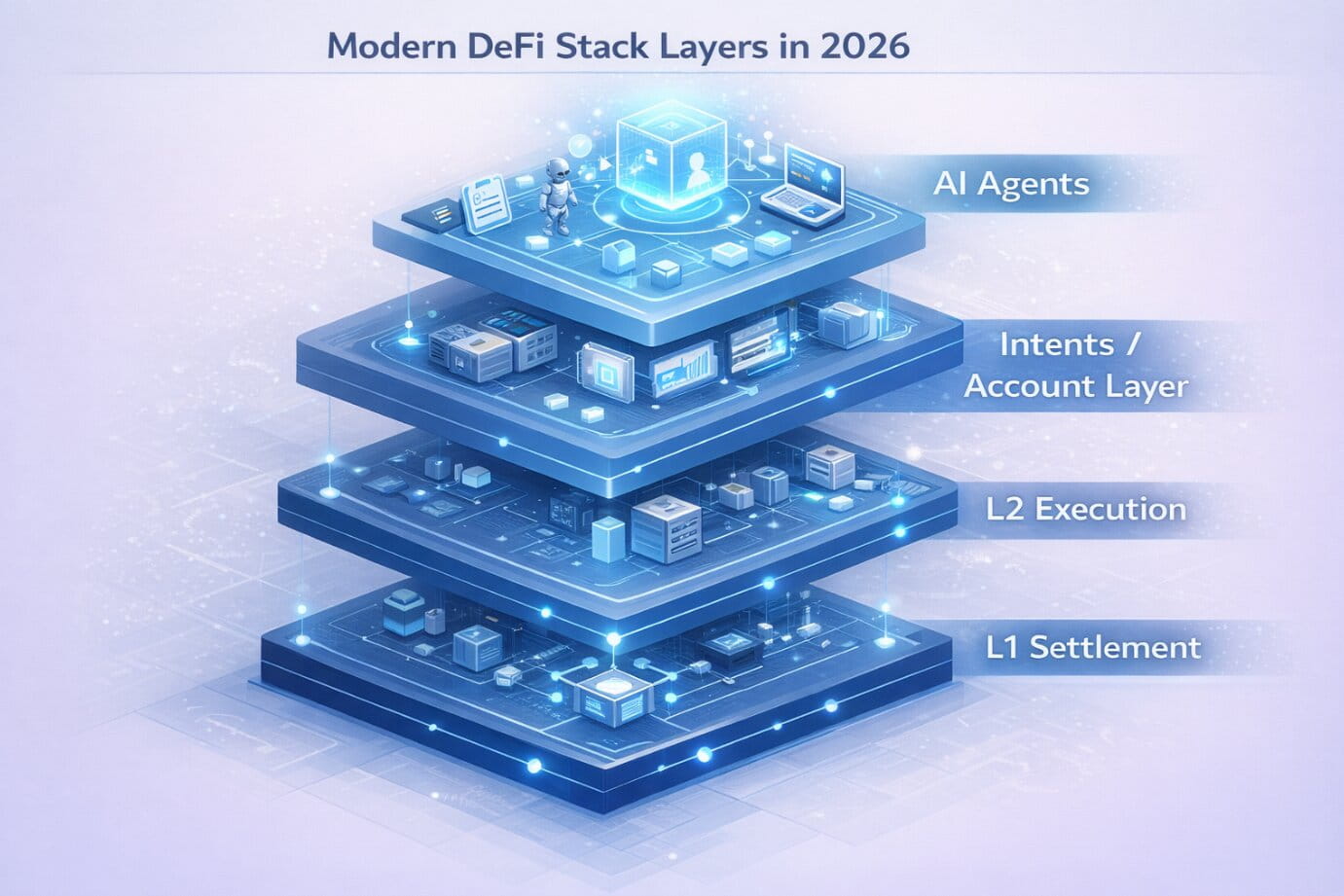

Intents, Account Abstraction and Onchain AI Agents

ERC-4337 smart accounts with session keys and paymasters let users express outcomes ('swap this for the best rate across any L2') rather than specifying individual transactions. Solver networks compete to fulfill the intent (Symbiosis). Layered on top, onchain AI agents are starting to monitor positions and rebalance within pre-approved risk bounds, reducing governance latency from weeks to hours. This introduces a new attack surface. Onchain AI agents can be faster and more powerful than human operators, and securing their access paths is becoming a 2026 security priority.

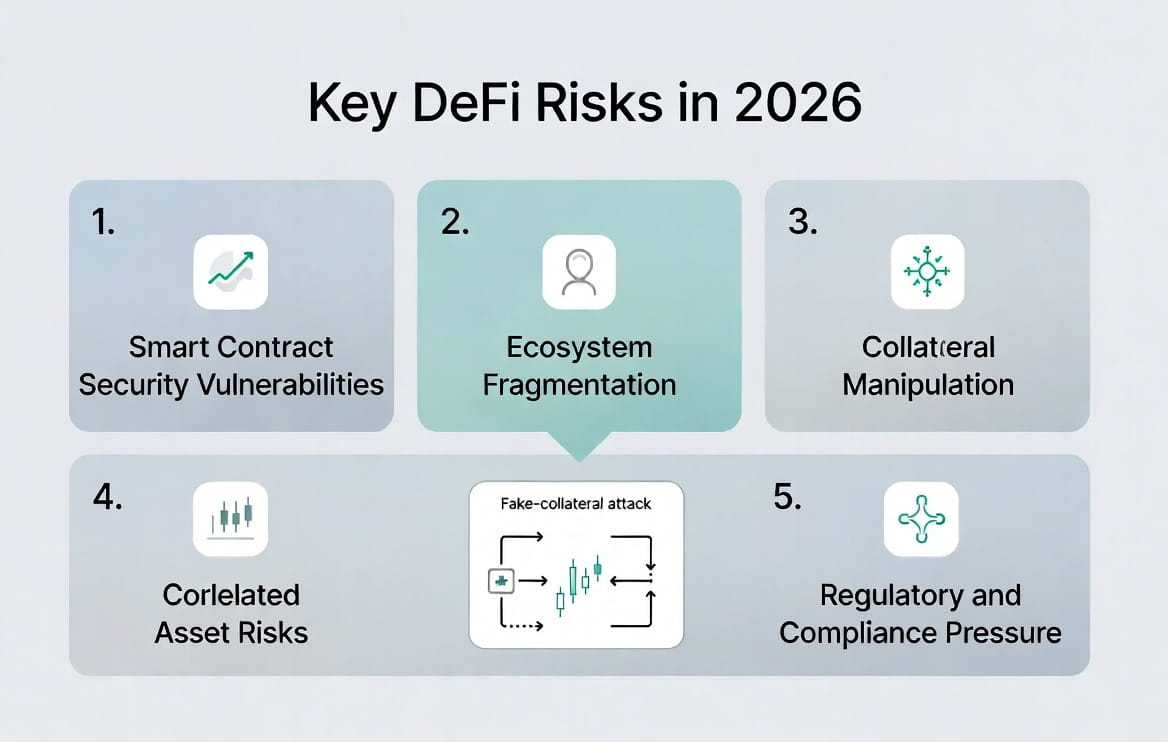

Risks and Limitations in 2026

The sector has matured, but risk has shifted rather than disappeared.

Security concentration.

Total crypto theft in 2025 reached roughly $3.4 billion, a record, but the headline number masks a more nuanced story for DeFi specifically. Onchain code security actually improved: DeFi-native losses per dollar of TVL declined even as TVL rebounded, a divergence from earlier cycles where growing deposits typically meant proportionally larger exploits. Where losses did occur, they shifted to the edges of the stack, driven mainly by compromised keys, wallet infrastructure attacks, and social engineering, while flash loan exploits remained the dominant code-level vector (~83%), with major incidents like the $223M Cetus exploit and $120M Balancer v2 hack reinforcing that pattern. Hallborn Chainalysis 2026 Crypto Crime Report

The remaining weak points are still familiar: oracle design, admin key management, and governance choke points, which is exactly the surface area where the Curve sDOLA and Drift incidents played out earlier.

Liquidity fragmentation. Dozens of L2s and app-chains now hold their own liquidity pools. Intent layers help, but fragmentation still raises slippage and makes risk correlations harder to see.

Correlated risk in restaking. Reusing the same collateral to secure multiple services creates hidden links. If one AVS fails catastrophically, cascading slashing could hit seemingly unrelated positions.

Execution concentration. As sophisticated flow routes through a small number of industrial venues like Hyperliquid and top L2s, market integrity depends more on the resilience of that narrow set. Pre-trade transparency suffers (DL News).

RWA-specific risks. Tokenized real-world assets import traditional market risk onchain. Redemption paths, oracle valuation of NAV, and legal enforceability of tokenized claims all matter more as the category grows.

Complexity and UX. Stacked yield strategies with LRTs re-deposited into lending protocols and then looped through Pendle create positions that even experienced users struggle to model.

Some Case Studies About Biggest Current Issues in DeFi 2.0: Artificial Collateral and Oracle Manipulation

A recurring exploit pattern in 2025 and 2026 has been attackers creating a low-liquidity asset they fully control, wash-trading it to an inflated price, and then using it as collateral inside a lending or margin system that accepts the oracle price as real. The pattern is not new, but it has grown more sophisticated and more expensive.

Hyperliquid JELLY (March 26, 2025). An attacker opened a $4.1M short on the illiquid JELLY memecoin, then pumped spot price more than 400% on external venues. Hyperliquid's HLP vault inherited the underwater short as positions liquidated, facing up to $13.5M in unrealized losses. Hyperliquid's validators force-closed all JELLY positions at the attacker's original entry rather than at the oracle-reported price, a move that saved the vault but exposed how few validators (four per set) stood between the protocol and that call Coindesk

Curve Finance sDOLA on LlamaLend (March 2, 2026). An attacker executed a donation-style manipulation on the sDOLA vault, shifting the sDOLA-to-DOLA exchange rate from roughly 1.188 to 1.358. The distortion did not break Curve's core contracts; it exploited the interaction between the oracle configuration and the liquidation logic, cascading through leveraged positions and liquidating users who had supplied sDOLA and borrowed crvUSD. Curve has said the fix involves a hardened oracle framework planned for LlamaLend V2 with stronger price validation against supply distortions (Bitcoin Ethereum News).

Drift Protocol on Solana (April 1, 2026). Drift lost approximately $285 million in roughly 12 minutes, the largest DeFi hack of 2026 so far. Attackers minted 750 million units of a fake token called CarbonVote Token (CVT), seeded a small Raydium pool with a few hundred dollars of liquidity, and wash-traded CVT to a manufactured price near $1. Drift's oracles picked up that artificial price as legitimate. A parallel six-month social engineering campaign, attributed with medium-to-high confidence to DPRK-linked actors, tricked Security Council members into pre-signing transactions using Solana's durable nonces feature. On April 1 those pre-signed transactions listed CVT as valid collateral with effectively infinite borrow limits, deposited 500 million CVT at the manufactured valuation, and drained real assets including USDC, JLP, SOL, cbBTC and WBTC in 31 rapid withdrawals (Chainalysis, TRM Labs).

The takeaway for users and builders is the same: protocols that accept a single-party-controlled asset as collateral are exposed to artificially pumped price feeds regardless of how well the underlying code is audited. Defenses include minimum liquidity thresholds, time-weighted price oracles, circuit breakers on collateral listing, timelocks on admin actions, and independent verification of pre-signed multisig transactions.

The Regulatory Shift That Changed Everything

For years, DeFi operated in a regulatory gray zone. That changed in 2025.

The GENIUS Act. Signed into law in July 2025, this is the first US federal framework for payment stablecoins (CoinNewsSpan). It requires 1:1 reserves in USD, short-term Treasuries, overnight repos or Fed credits. Issuers must publish monthly audited reserve reports, and paying interest to stablecoin holders is explicitly banned (Phemex breakdown). The OCC published its 376-page implementing rule on February 25, 2026, with final regulations targeted for July 2026.

MiCA. The EU's Markets in Crypto-Assets regulation is now fully operational. Stablecoin issuers must be authorized by July 1, 2026, or face exclusion from EU markets. By early 2026, 14 issuers held MiCA authorization across seven member states, with around 20 compliant stablecoins in circulation (KuCoin: Stablecoin Regulation 2026). USDC transaction volume in Europe jumped 337 percent in H1 2025 after Circle secured MiCA compliance (CoinNewsSpan).

Global alignment. Hong Kong expects its first Stablecoin Ordinance licenses in Q1 to Q2 2026. Singapore finalized its Single-Currency Stablecoin framework. Brazil classified stablecoin operations as foreign exchange activities in November 2025. The OECD's Crypto-Asset Reporting Framework (CARF) begins producing cross-border exchange reporting from 2027 (Sumsub: Crypto Regulation in 2026).

For DeFi, the regulatory environment is a double-edged sword. It opens the door to institutional participation through compliant RWA rails. It also raises questions that regulators have not fully answered, including what counts as sufficiently decentralized to escape MiCA's reach.

What Comes After DeFi 2.0

The next phase is already forming, whether it is labeled DeFi 3.0 or not. The direction is clear: institutional integration, RWA-backed collateral, and automation driven by AI systems.

Three structural shifts define this transition. First, user experience is moving toward bank-level simplicity while remaining non-custodial and fully auditable (Symbiosis). Second, liquidity is consolidating into unified layers where cross-chain complexity is abstracted through intent-based execution and solver networks. Third, credit markets are maturing around tokenized Treasuries and private debt, introducing yield profiles that are fundamentally more predictable than anything native crypto has produced so far.

DeFi 2.0 did not fail; it normalized its own innovations. Sustainable liquidity, capital efficiency, and emission-independent yield are no longer differentiators, they are baseline requirements.

The real question is no longer how DeFi sustains itself, but whether it can integrate with global financial infrastructure without compromising its core property: permissionless access. If that balance breaks, DeFi becomes just another backend for traditional finance. If it holds, it becomes the infrastructure layer of it.

This is where Decentralized Finance stands today and where it is heading next. The trajectory is set. What remains uncertain is not the direction but who will survive the transition. @Kripto Raptor

Frequently Asked Questions

Is DeFi 2.0 still a relevant term in 2026?

The label has faded. Most of what DeFi 2.0 described, protocol-owned liquidity, sustainable yield, better capital efficiency, has been absorbed into DeFi generally. Analysts and builders now talk about specific categories like restaking, RWA, perp DEXs, and intent layers rather than a unified 2.0 narrative.

How big is DeFi in 2026?

Total value locked sits at roughly $130 to $140 billion across all chains, with Ethereum holding the majority (CoinLaw, DefiLlama). The top five protocols by TVL (Aave, Lido, EigenLayer, Sky and Uniswap) account for more than half of that total.

What is Protocol Owned Liquidity and does it still work?

POL is when a protocol owns its liquidity positions directly rather than paying external LPs to supply them. OlympusDAO popularized the bonding model (Olympus Docs). The approach still works for certain treasuries, though it has become one tool among many rather than a defining feature of the sector.

What replaced yield farming as the main yield source?

Real-world asset yields (tokenized Treasuries paying 3.5 to 4 percent), liquid staking (base ETH staking yield plus restaking premium), stablecoin lending on Aave and Morpho, and fixed-rate products on Pendle now supply most sustainable onchain yield (KuCoin RWA). Emissions-driven farming still exists but attracts more cautious capital than it did in 2021.

Are tokenized real-world assets the same as stablecoins?

No. Stablecoins are dollar-pegged payment instruments. Tokenized RWAs represent claims on offchain assets like Treasuries, money market funds, tokenized stocks, private credit or real estate. They often pay yield, which regulated stablecoins generally cannot under the GENIUS Act and MiCA (Phemex).

Is DeFi safer in 2026 than in previous cycles?

Onchain code security has improved materially, and faster governance response has helped protocols recover funds or contain damage after attacks. The result is a clear divergence from past cycles: DeFi-native losses per dollar of TVL are down even as deposits have rebounded. But the attack surface has shifted rather than shrunk. Off-chain vectors like compromised private keys, supply-chain exploits targeting wallet and deployment infrastructure, and oracle-based collateral manipulation now drive most large losses. The Drift Protocol incident of April 2026, where attackers combined a wash-traded fake token, a manipulated oracle feed, and a months-long social engineering campaign against Security Council signers to drain roughly $285 million, is the clearest example so far that a well-audited protocol can still be compromised through its human and governance layers. (Chainalysis: lessons from Drift).

Will the GENIUS Act affect DeFi protocols?

Directly, it regulates stablecoin issuers, not DeFi protocols. Indirectly, it reshapes which stablecoins dominate (USDC is well-positioned, Tether's status in regulated markets is uncertain), which affects collateral choices across DeFi (Phemex: GENIUS Act Explained).

What is the biggest DeFi trend to watch in 2026?

Real-world assets as onchain collateral, combined with perpetual DEX growth and the maturation of restaking, are the three trends that matter most. Each brings more capital, more regulation, and more institutional participation than DeFi previously had access to.